7 Loan Management Trends That Will Shape 2026

Loan management is evolving faster than at any point in the past decade.

The 2026 Lending Operations Benchmark Report shows a clear shift: lenders aren’t just digitising paperwork – they’re rethinking how decisions, data, and compliance fit together.

Borrowers expect answers in hours, regulators expect stronger auditability, and operations teams need tools that scale without adding complexity. For specialist lenders handling hundreds or thousands of loans, these pressures are even sharper.

Below, we break down seven trends that will define loan management in 2026 – and what they mean for lenders aiming to operate faster, smarter, and with greater control.

1. Speed Becomes a Core Risk & Performance Metric

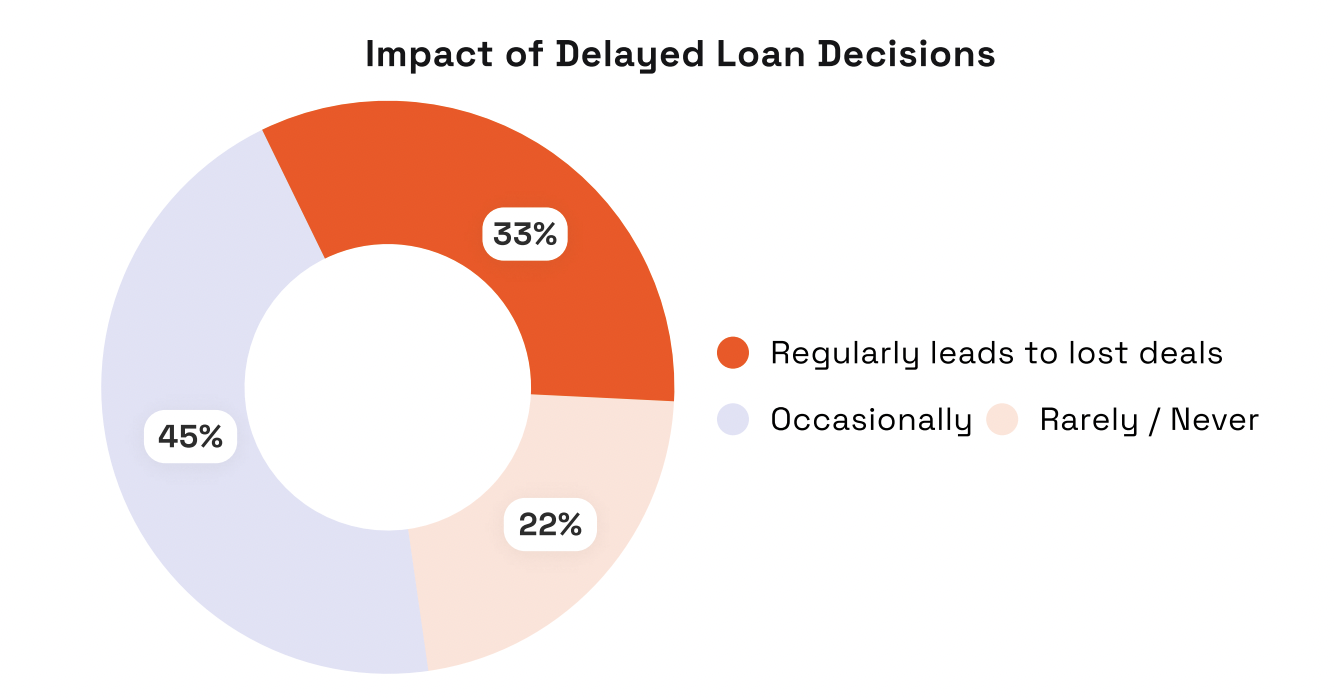

Speed is no longer treated as a CX bonus or a competitive advantage – it’s becoming a core operational KPI.

Our research shows lenders increasingly measuring time-to-decision with the same seriousness as default rates or portfolio performance. That shift is driven by three forces:

- Borrowers abandon slow processes faster than ever

- Faster decisions correlate with higher conversion

- Delays introduce real revenue and pipeline risk

In 2026, speed becomes a direct indicator of operational health.

Slow decisions are no longer just an inconvenience – they’re a risk.

2. Compliance Moves Inside the Workflow

Compliance has historically been a separate track, often managed by tools or processes that sit outside core lending operations. That separation is now one of the biggest bottlenecks.

We’ll see more lenders:

- Embedding KYC, AML, and verification directly into digital workflows

- Automating standard checks and routing only true exceptions

- Treating compliance as an always-on layer, not a sequential step

This doesn’t weaken oversight – it strengthens it by reducing manual variation and making audit trails cleaner.

Compliance becomes faster and safer when it’s part of the workflow, not a detour.

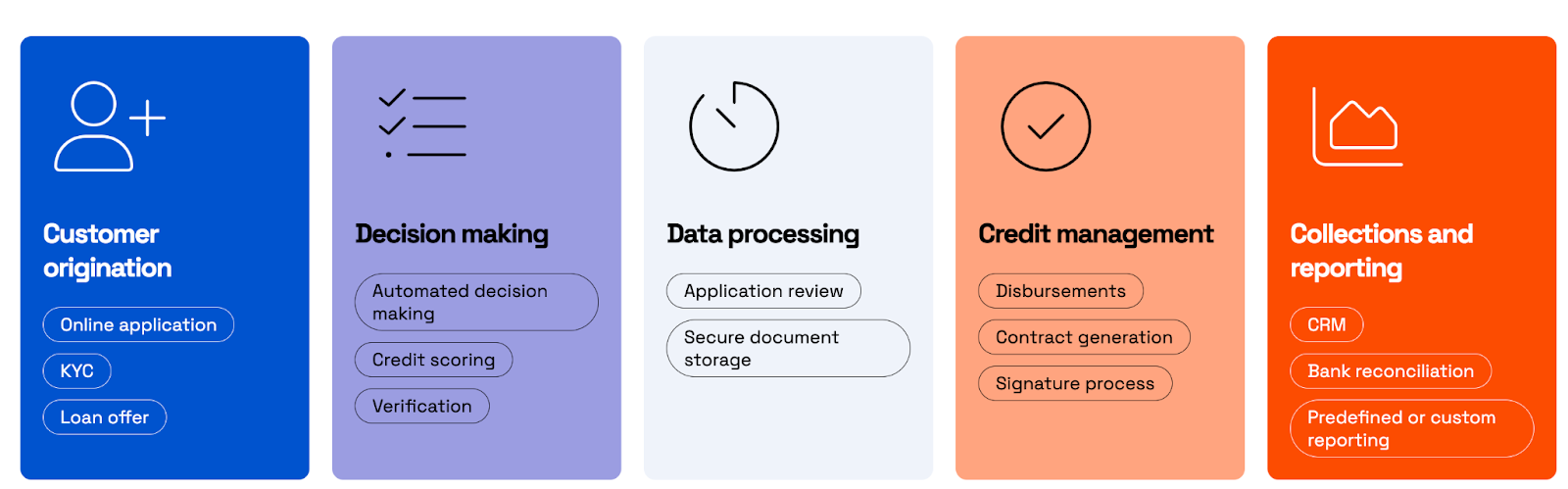

3. End-to-End Automation Replaces Point Solutions

Most lenders already have isolated tools for credit checks, e-signing, or document generation. The challenge is that these tools don’t talk to each other.

The trend for 2026 is clear:

Automation must span the whole loan lifecycle, not individual tasks.

Lenders are now prioritising:

- Workflow orchestration over new standalone tools

- Automation that connects origination → underwriting → servicing

- System design that reduces handoffs, not adds more

The real efficiency gains come when automation is end-to-end, not when it’s bolted on in pieces.

4. Configurable Systems for Specialist Lending

Specialist lenders operate differently from mainstream retail banks.

Product structures are more complex, underwriting logic is more nuanced, and workflows often require exceptions that off-the-shelf systems simply can’t support.

In 2026, lenders will increasingly demand platforms that:

- Adapt to niche products without custom builds

- Allow rapid configuration of workflows and rules

- Support new product launches without months of development

Configurability becomes essential – not a luxury.

Rigid systems will be replaced by platforms designed around complexity, not simplicity.

5. Unified Data as the Foundation for Decisioning

Disconnected data is one of the largest hidden costs in lending.

When teams can’t see the same information in real time, they can’t move fast – and they can’t move confidently.

Unified data solves this by:

- Eliminating the need for manual reconciliation

- Providing a single source of truth for borrower, credit, and compliance data

- Powering real-time dashboards for pipeline and portfolio monitoring

In 2026, unified data becomes the foundation that makes everything else possible – including speed, accuracy, and compliance integrity.

6. Ops, Risk, and IT Working From One System

Operational silos create friction. Friction slows decisions. And slow decisions lose business.

The highest-performing lenders in our research have one thing in common:

Their teams operate from the same system, not from shared inboxes or disconnected tools.

This shift:

- Reduces wait times between teams

- Makes status updates instant rather than requested

- Aligns underwriting, risk, operations, and compliance in one environment

When everyone sees the same information at the same time, decisions naturally accelerate – without pushing teams harder.

7. Platforms Become Partners, Not Vendors

Specialist lenders don’t just need software – they need ongoing support, rapid changes, and hands-on adaptation as products, markets, and rules evolve.

In 2026, the industry trend is clear: Lenders expect their loan management platforms to act like a long-term operational partner, not a tool provider.

This means:

- Continuous platform evolution

- Hands-on technical support

- Workflow design help

- Integrations built and maintained by the vendor

- A technology partner that understands lending, not just software

For many lenders, this relationship effectively replaces the need for a large internal IT team.

The Shift From Digital Tools to Connected Operations

Loan management in 2026 isn’t about “going digital” – that’s already happened.

The challenge now is connecting everything that’s digital.

The lenders that lead the next phase of the industry will be the ones that:

- Treat speed as a system outcome

- Embed compliance into workflows

- Replace manual steps with end-to-end automation

- Operate from shared, connected platforms

- Build around unified data

When systems, teams, and processes work together, speed becomes natural – not forced.

And in a market where borrowers expect decisions in hours, not days, that difference is what will define the winners of 2026.

Want to reduce bottlenecks and accelerate decisions? Book a demo and discover how LendFusion connects origination, underwriting, and compliance into one seamless system built for speed.

Andres Valdmann, CEO

Andres is the Chief Executive Officer at LendFusion. Andres has 15 years of experience in fintech and loan management software and has a proven track record in helping companies hit their growth goals.

Connect with Andres on LinkedIn.