LendFusion vs. HES FinTech: Which Loan Management System Delivers More Value?

If your current loan system feels like duct tape and workarounds, chances are you’ve looked at LendFusion and HES FinTech. But which one actually fits your team?

Both vendors are known for innovation, but they take very different approaches. HES FinTech is often positioned as a custom development partner that builds bespoke lending platforms from scratch.

LendFusion, by contrast, is a modular, configurable platform that gives specialist lenders speed and control without the overhead of long, expensive dev projects.

In this guide, we’ll break down how the two compare – from automation to compliance, onboarding, and pricing – so you can decide which LMS actually fits your operating model.

Why Compare LendFusion and HES FinTech?

Both platforms promise automation, modern workflows, and a better borrower experience. But they’re not interchangeable.

- HES FinTech shines when you need a fully custom-built platform, with developers tailoring every screen, rule, and flow.

- LendFusion excels when you want a ready-to-go system that’s configurable and built specifically for regulated specialist lenders.

If you’re weighing speed against customization – and predictability against flexibility – this comparison will help you cut through the noise.

LendFusion vs. HES FinTech: Head-to-Head Comparison

Here’s how the two platforms stack up across the features that matter most.

| Feature | LendFusion | HES FinTech |

|---|---|---|

| Origin | Global hosting (GDPR-first, client-selected AWS region) | Global dev-focused vendor, custom builds |

| Focus | Specialist lending: bridge, development, asset-backed, private credit | Full-suite lending systems, built bespoke across industries |

| Ease of Use | Modular, intuitive UI for operators | Depends on scope; UI built per client spec |

| Automation | Rules-based decision engine, audit trails, end-to-end workflows | Strong automation, but often requires custom development |

| Data Ownership | Full access via AWS S3, no lock-in | Vendor-hosted; data portability varies by project |

| Compliance | GDPR-first, audit-ready | Customizable compliance; varies by build |

| Deployment | Cloud-native, fast go-live (2–3 months typical) | Project-based builds (longer timelines, higher cost) |

| Support | Direct access to implementation team, named success manager | Enterprise-style support, but tied to custom project scope |

| Pricing | Transparent flat monthly fee, no per-seat charges | Quote-based, project pricing (higher upfront cost + ongoing development fees) |

LendFusion vs. HES FinTech: How to Decide

If you’ve narrowed your shortlist to these two platforms, the next step is weighing not just features, but implementation style and long-term fit.

Here’s where the differences become clearest:

Choose LendFusion if you want:

1. Faster Go-Live With Configurability

Most lenders can launch in under 3 months, with minimal disruption. Unlike rigid template systems or fully bespoke builds, LendFusion combines speed with deep configurability, letting you adapt loan products, fees, and workflows without developer bottlenecks or runaway costs.

2. Compliance and Control From Day One

Designed for global deployment, LendFusion lets each client choose their preferred AWS region while remaining GDPR-first by default. The platform includes role-based access, audit trails, and regulator-ready reporting. Lenders retain full ownership of their data, with open APIs and optional direct S3 access ensuring no vendor lock-in or hidden restrictions.

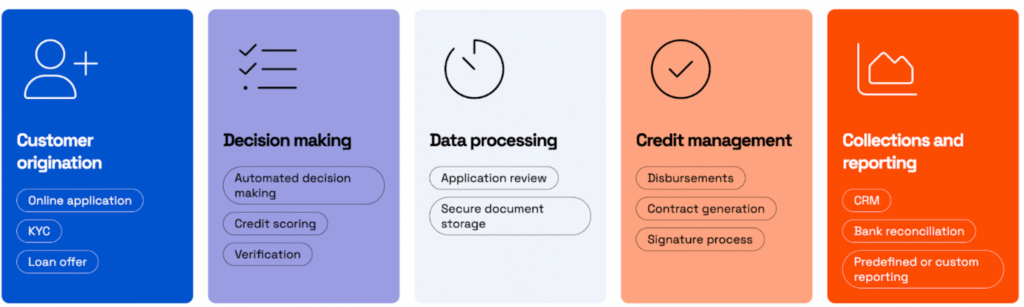

3. End-to-End Lending Lifecycle in One Platform

From origination and underwriting to disbursements, servicing, and collections, LendFusion covers every stage natively. No bolt-ons, no patchwork tools – just one unified system that grows with your lending model.

Choose HES FinTech if you want:

1. Fully Custom-Built Lending Systems

HES FinTech approaches every engagement like a development project. They design and deliver tailored platforms built from scratch, which means you can specify exactly how the borrower portal, risk models, and servicing logic should function – but with longer delivery times.

2. Broad Lending Coverage

HES has worked with lenders across diverse verticals, from payday and leasing to BNPL and microfinance. This breadth makes it attractive if you require highly specialized product support, even if it comes with additional development overhead and higher upfront investment.

3. Deep Hands-On Collaboration

HES acts more like a dev partner than a pure SaaS vendor. Their teams collaborate closely to scope, build, and maintain your platform. While this offers high flexibility and tailored outcomes, it also means heavier reliance on their resources and higher total ownership cost.

Still weighing your options? You might also like our guide on the best HES FinTech alternatives – a deeper dive into other platforms worth considering.

Which LMS Meets Your Lending Needs?

| Business Need | LendFusion | HES FinTech |

|---|---|---|

| Fast, low-risk onboarding | Typical go-live in under 3 months with zero downtime | Project-based builds; longer timelines |

| Specialist lending workflows | Purpose-built for bridge, development & asset-backed models | Possible, but requires custom build |

| Data control & compliance | Global hosting, GDPR-first, full data access | Compliance options available, varies per build |

| Transparent pricing | Flat monthly fee, all features included | Project-based, higher upfront investment |

| Fully bespoke solution | Configurable but not from-scratch builds | Custom-built, white-label platforms from the ground up |

| Best fit for | Scaling specialist lenders (£10M–£100M portfolios) | Lenders with niche products & budget for custom builds |

Both platforms can deliver powerful results, but they do so in very different ways.

Your choice will depend on whether you want a SaaS-style product you can configure today – or a bespoke build tailored for tomorrow.

Final Thoughts: LendFusion vs. HES FinTech

Both LendFusion and HES FinTech bring strong capabilities to the table, but their value propositions diverge.

LendFusion is best for lenders who want speed, compliance, and configurability without getting trapped in endless development cycles or unpredictable costs.

HES FinTech, on the other hand, appeals to those who prioritize a fully custom-built platform and can afford the trade-offs of longer timelines and higher budgets.

Ultimately, the choice isn’t just about features – it’s about operating philosophy.

Do you want a configurable platform that gets you live quickly and grows with your lending model, or a bespoke system that requires heavy investment and ongoing development?

For most scaling lenders who need resilience, speed, and control, LendFusion offers a clearer and lower-risk route to long-term success.

Ready to see why many lenders choose LendFusion over HES FinTech?

Book a personalized demo today and discover how a modern, configurable platform can replace fragmented tools and heavy custom builds – without disrupting your borrowers or your team.

Vahuri Voolaid, COO

Vahuri is the Chief Operations Officer at LendFusion. Vahuri has 9 years of experience in fintech with loan management software as a product owner and an MBA with a specialisation in IT management.

Connect with Vahuri on LinkedIn.