The Consumer Lending Process Explained : From Application to Repayment

TL;DR The consumer lending process covers every step from a borrower’s initial application through to full repayment – including identity checks, credit decisioning, contract signing, disbursement, and collections. For growing lenders, each stage is an opportunity to reduce manual work, speed up decisions, and improve borrower experience.

Consumer lending is one of the most process-intensive activities in financial services. From the moment a borrower submits an application to the final repayment, lenders must navigate a tightly orchestrated sequence of checks, decisions, communications, and transactions – all while staying compliant, managing risk, and delivering a seamless borrower experience.

For new and growing lenders, understanding each stage of the process is essential – not just to get it right, but to identify where efficiency gains are possible. This guide walks through the full consumer lending lifecycle and highlights how technology, particularly loan management software, is reshaping each step.

What Is Consumer Lending?

Consumer lending refers to the extension of credit to individual borrowers for personal use. This includes personal loans, auto loans, buy now pay later (BNPL) arrangements, and other forms of retail credit.

Unlike business lending, consumer lending typically involves higher volumes of smaller-value loans, making operational efficiency especially critical.

The stakes are high: inefficient processes mean slower approvals, frustrated borrowers, higher default rates, and operational costs that don’t scale.

The lenders growing fastest are the ones who have systematized each stage – and increasingly, automated it.

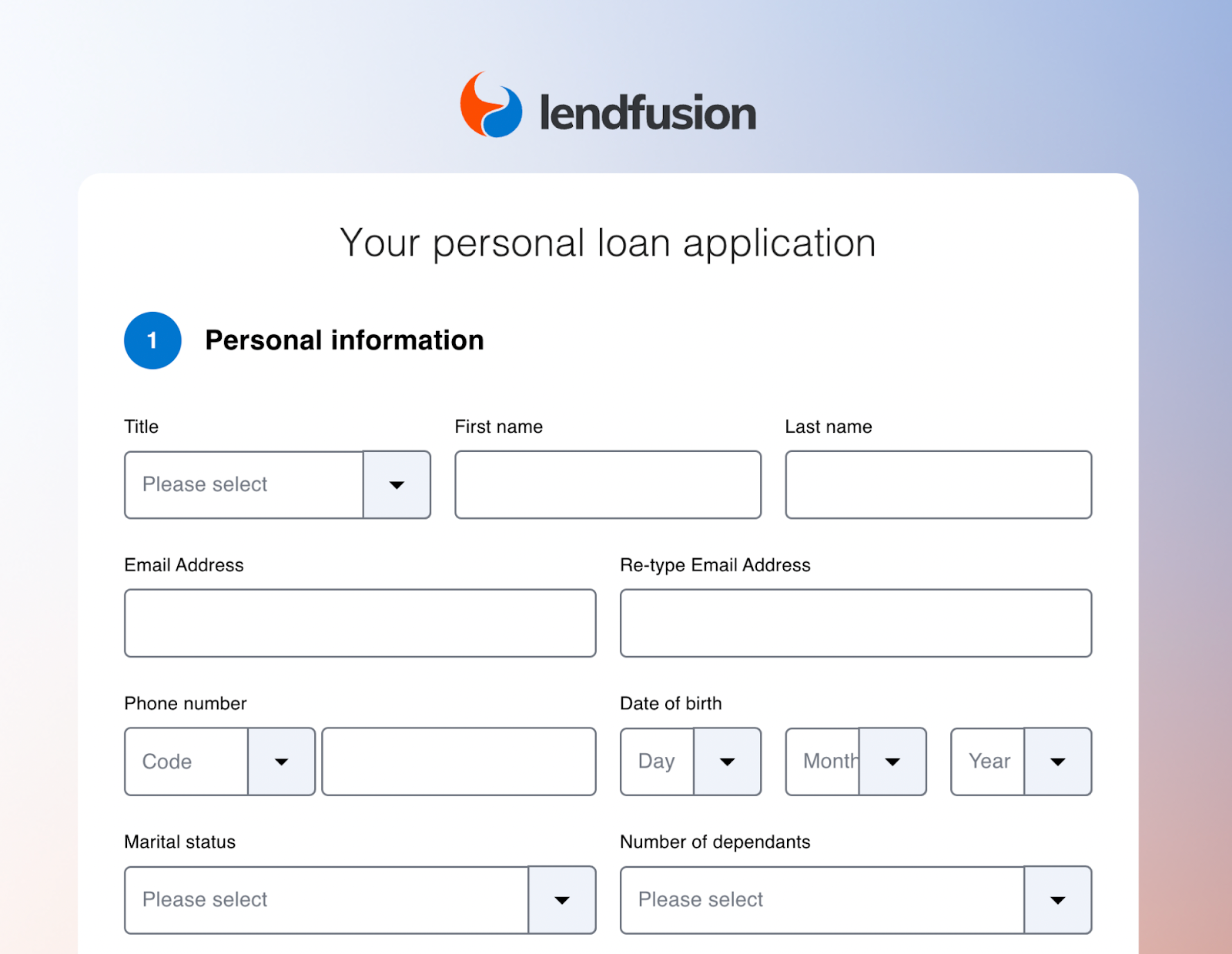

1. Loan Application

Everything begins with the borrower.

Whether through a website, a mobile app, or an embedded checkout flow, the application is the first point of contact – and first impressions matter.

A clunky, lengthy application process increases abandonment rates before a single creditworthiness check takes place.

A modern consumer loan application typically captures:

- Personal details (name, address, date of birth)

- Employment and income information

- Loan purpose, amount, and preferred repayment term

- Consent for credit checks and data processing

Lenders using platforms like LendFusion can deploy customizable online application forms that feed directly into their loan management system – eliminating manual data entry and reducing errors from the outset.

2. Identity Verification (KYC)

Before a lender can assess creditworthiness, they must verify the borrower is who they say they are. Know Your Customer (KYC) checks are a regulatory requirement in most markets, designed to prevent fraud, money laundering, and identity theft.

KYC checks typically involve:

- Document verification (passport, driving licence, national ID)

- Address verification

- Sanctions and PEP (Politically Exposed Persons) screening

- Biometric or liveness checks in some cases

Integrating KYC directly into the lending workflow – rather than managing it as a separate process – dramatically reduces the time from application to decision and improves the borrower experience.

3. Credit Assessment and Decisioning

This is the core risk management stage – where a lender determines whether to approve, decline, or refer an application for manual review. It draws on multiple data sources to build a picture of the borrower’s financial health and repayment ability.

Inputs typically include:

- Credit bureau reports (e.g. Experian, Equifax, TransUnion)

- Open banking data for real-time income and expenditure analysis

- Internal scoring models based on the lender’s own portfolio data

- Debt-to-income ratios and affordability calculations

Modern decision engines – like the one built into LendFusion – allow lenders to configure their own approval rules, risk thresholds, and referral criteria without writing a single line of code.

Applications that meet your criteria are auto-approved; those that don’t can be automatically declined or flagged for a human underwriter.

The speed of decisioning has become a major competitive differentiator in consumer lending. Borrowers who receive an instant decision are significantly more likely to proceed than those left waiting.

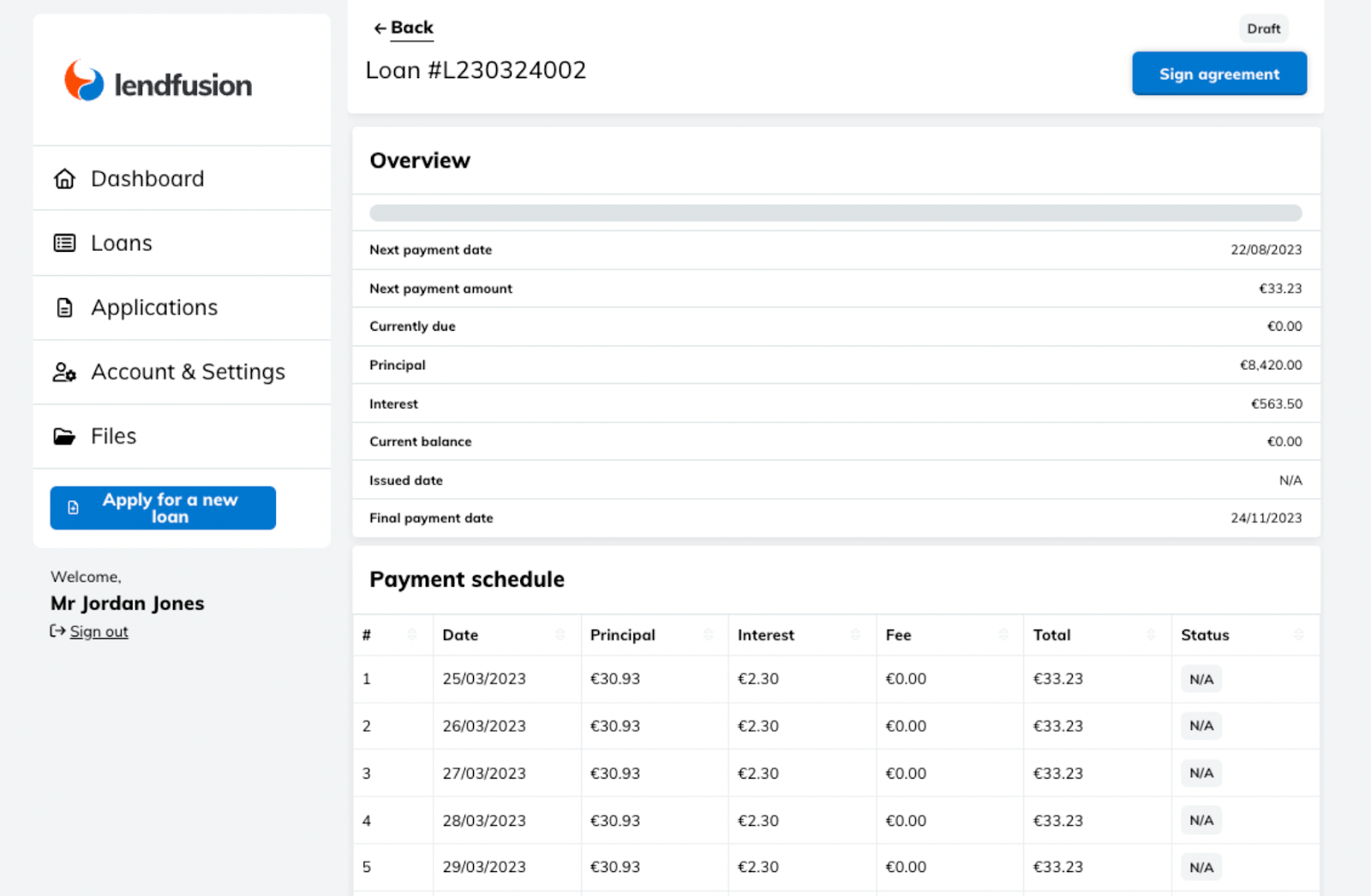

4. Loan Offer and Agreement

Once approved, the borrower is presented with a formal loan offer detailing the approved amount, interest rate, repayment schedule, and any applicable fees. This is an important communication touchpoint – clarity here reduces disputes and defaults later.

After acceptance, a loan agreement is generated and must be signed. E-signature capabilities embedded in the lending workflow remove the need for physical paperwork, dramatically accelerating this step – particularly important for digital-first consumer lenders.

Automated communication tools can send the offer via email or SMS, track whether it has been opened and accepted, and trigger the next step automatically – reducing the manual chasing that bogs down many lending teams.

5. Disbursement

With the agreement signed, the lender disburses the funds to the borrower.

The speed of this step is again a key factor in borrower satisfaction – same-day or next-day disbursement has become an expectation for many consumer products.

Disbursement processes should be directly connected to the lender’s payment infrastructure, with automatic reconciliation to the loan book. LendFusion integrates with leading payment providers including Stripe, GoCardless, and others – enabling seamless disbursement without manual bank transfers.

6. Repayment Collection and CRM

Once funds are disbursed, the focus shifts to managing the ongoing loan relationship. This includes collecting scheduled repayments, sending timely reminders, tracking missed payments, and managing the customer relationship throughout the loan term.

A well-run repayment collection process includes:

- Automated payment collection via direct debit or card

- Pre-payment reminders via email or SMS to reduce missed payments

- Automatic late payment fees where applicable

- Early arrears management workflows to catch problems before they escalate

- A 24/7 borrower self-service portal to view balances and repayment schedules

A self-service borrower portal – like the one included in LendFusion – significantly reduces inbound support queries, freeing up your team to focus on higher-value work.

7. Reporting, Compliance, and Audit

Running a consumer lending operation means operating within a regulatory framework – whether that’s the FCA in the UK, CFPB in the US, or local equivalents.

Every stage of the lending process must be documented, auditable, and reportable.

Loan management platforms maintain a full audit trail automatically – logging every application update, decision, communication, and transaction in real time. This not only satisfies regulatory requirements but gives lenders full visibility over their portfolio performance, arrears levels, and operational metrics.

Predefined and custom reporting capabilities allow lenders to monitor the health of their loan book and spot trends before they become problems – without having to export data into spreadsheets and build reports manually.

Why Manual Processes Hold Lenders Back

Many lenders – especially those in the early stages of growth – piece together their lending process using spreadsheets, email, and disconnected tools. This approach works up to a point, but it breaks down as volume increases. Common problems include:

- Slow application processing that frustrates borrowers and increases abandonment

- Data entry errors that cause compliance issues or incorrect loan terms

- No single view of the loan book, making portfolio management reactive rather than proactive

- Teams spending time on admin instead of sales or underwriting

- Difficulty launching new products or entering new markets without rebuilding processes from scratch

Planet42, one of LendFusion’s longest-standing customers, grew from a €0 loan portfolio to €100 million – and 200+ employees – without rebuilding their back office. The platform they started on scaled with them.

Building a Consumer Lending Process That Scales

The consumer lending process isn’t just a series of steps – it’s the engine of your business. Every inefficiency, manual hand-off, or disconnected tool is friction that costs you time, money, and borrower trust.

The lenders growing fastest are those who’ve invested in a platform that handles the end-to-end process in one place: from online application and KYC through automated decisioning, contract generation, disbursement, collections, and reporting.

Not just because it’s more efficient – but because it gives them the operational foundation to launch new products, enter new markets, and scale their team without adding complexity.

Whether you’re currently operating on spreadsheets or transitioning from a legacy system, the right loan management software should feel like a partner in growth – not just a tool.

Ready to Modernize your Consumer Lending Process?

LendFusion is a loan management platform built for growing lenders – with automated decisioning, seamless integrations, and a team that stays hands-on from onboarding through scale. Go live in weeks, not months.

Vahuri Voolaid, COO

Vahuri is the Chief Operations Officer at LendFusion. Vahuri has 9 years of experience in fintech with loan management software as a product owner and an MBA with a specialisation in IT management.

Connect with Vahuri on LinkedIn.