How to Reduce Loan Decision Times (The #1 Biggest Operational Bottleneck)

Borrowers expect faster decisions than ever.

In our 2026 Lending Operations Benchmark Report, 68% of lenders said borrowers expect a same-day decision.

Yet despite this awareness, one in three lenders still take three days or more to approve a loan.

This isn’t because lenders lack urgency or insight. It’s because the operational foundations beneath lending – workflows, systems, and compliance structures – were never designed for the expectations lenders are now asked to meet.

This article explores why delays still happen, what slow decisioning is really costing lenders, and how the fastest lenders are breaking away from the pack.

The Expectation Shift Lenders Can’t Ignore

Years ago, waiting a few days for a loan decision felt normal. Today, it feels outdated. Borrowers compare lenders to every other digital interaction in their lives – whether it’s opening a bank account in minutes or receiving instant credit at checkout.

This shift isn’t theoretical. It shows up immediately in borrower behavior. When lenders take too long, applicants don’t sit and wait – they apply elsewhere, accept a faster offer, or simply drop out of the process altogether.

The market now moves at the speed of the borrower, not the speed of the institution. And lenders who fail to match that pace feel the consequences quickly.

Why Decisions Still Take Days

The slowest part of lending rarely happens in underwriting. Instead, delays come from something far more foundational: the way information moves (or doesn’t move) through the organisation.

At most lenders, compliance steps sit outside core workflows. KYC, AML, and document checks often require manual review or are spread across several systems that don’t talk to each other. What should take minutes turns into hours – and then into days.

Manual work compounds the problem. Many lenders still rely on spreadsheets, shared inboxes, or partially connected systems that require someone to copy information from one place to another. When volumes rise, these small inefficiencies stack up quickly.

And beneath all of this lies infrastructure that was never built for real-time lending. Legacy systems operate linearly: step one, then step two, then step three. Modern borrowers expect everything to happen at once.

The result is predictable – delays that aren’t caused by risk assessment, but by the operational scaffolding around it.

The Real Cost of Slow Decisions

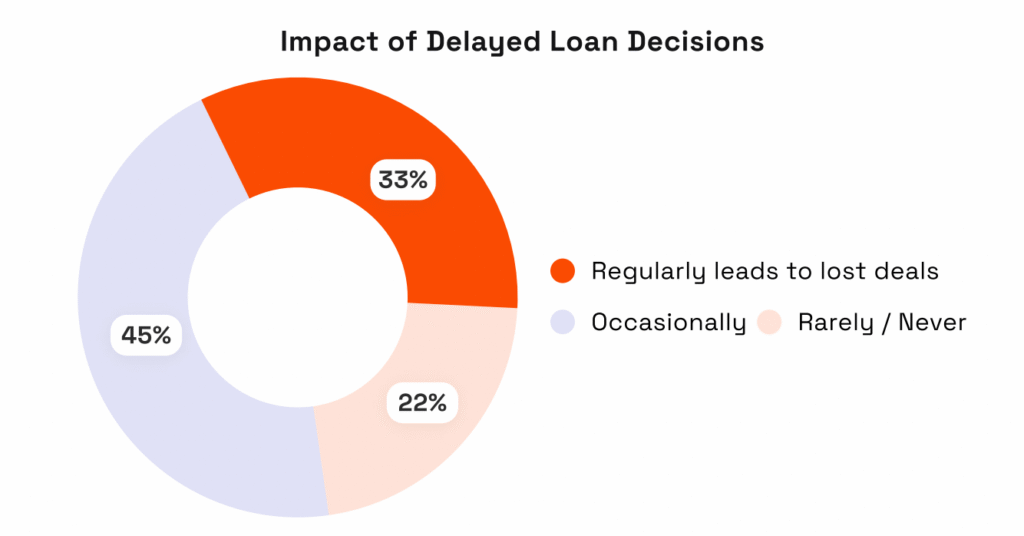

Speed isn’t just a customer-experience metric. It’s a revenue metric. When decisions lag, deals are lost – and the data confirms this. One in three lenders say they regularly lose deals due to slow turnaround times, and another 45% say it happens occasionally.

But the cost extends well beyond missed applications. Slow decisions erode trust. Borrowers start to question whether the lender is reliable or organised. That perception doesn’t stay contained to a single interaction – it affects retention, referrals, and brand credibility.

There’s also the operational cost: more follow-ups, more manual work, more exceptions to manage, and more staff hours required to move applications across fragmented processes.

In short: being slow doesn’t just hurt growth. It quietly makes everything more expensive.

What the Fastest Lenders Are Doing Differently

The lenders who consistently deliver decisions in hours aren’t doing it because they’ve cut corners or hired more people. They’re doing it because their operations are connected – structurally, technologically, and cross-functionally.

Across the highest-performing institutions in our study, several themes consistently emerged.

They treat data as a single flow, not a series of handoffs

Fast lenders don’t chase information through disconnected systems.

Borrower details, credit data, documents, and compliance signals all sit in one environment. That removes friction long before underwriting even begins. It also reduces the cognitive load on teams – underwriters focus on decisions, not document-tracking.

Compliance is built directly into the workflow

When compliance runs in parallel – not as a separate track – turnaround times compress naturally.

Top lenders embed KYC, AML, and verification steps into the digital workflow so nothing needs forwarding or separate review unless flagged. This strengthens control by making checks consistent and auditable.

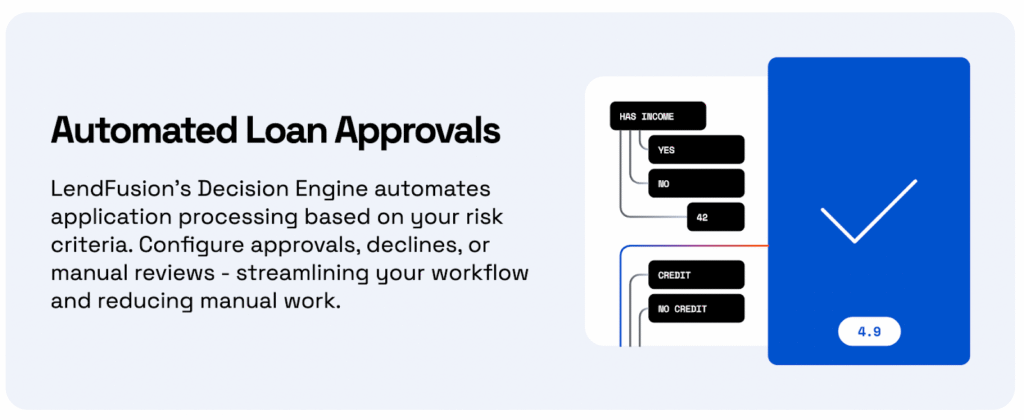

Automation supports human decisioning rather than replacing it

High-performing lenders automate the predictable parts of underwriting – not the judgment-heavy parts. Clear cases move through rules engines. Borderline cases go to experienced underwriters.

This combination keeps quality high while dramatically reducing the volume of manual decisions.

Teams work from one system, not a shared inbox

When operations, risk, compliance, and underwriting all work in the same environment, delays disappear almost unintentionally. Teams aren’t waiting on replies or status updates – everyone sees the same information in real time.

The result is not just faster decisions. It’s an operation that scales without adding complexity.

How LendFusion Helps Lenders Make This Shift

LendFusion was designed for specialist lenders who need decision speed but operate in high-volume, complex environments where spreadsheets, legacy systems, and bolt-on tools create friction.

By unifying origination, underwriting, compliance, servicing, and reporting in one platform, LendFusion removes the fragmentation that slows lenders down.

With LendFusion:

- Compliance checks run inside the workflow

- Data moves automatically end-to-end

- Underwriting rules accelerate predictable cases

- Manual steps shrink

- Approval times fall naturally

Many lenders see approval times fall sharply after consolidating their processes in loan management software – not because they add more tools, but because they finally connect them.

Faster Decisions Are the Outcome of Connected Operations

The lenders winning in 2026 aren’t winning because they’ve improved one step of their process. They’re winning because their systems, teams, and workflows operate as one integrated motion.

When lending operations become connected, speed stops being something you chase – and becomes something that happens by design.

The next era of progress in lending won’t come from marginal system upgrades or isolated automation projects. It will come from eliminating the gaps between systems altogether.

When systems work together, speed becomes strategy.

Ready to shorten your decision times? Book a personalized demo and see how LendFusion helps lenders cut approvals from days to hours – without adding complexity.

Andres Valdmann, CEO

Andres is the Chief Executive Officer at LendFusion. Andres has 15 years of experience in fintech and loan management software and has a proven track record in helping companies hit their growth goals.

Connect with Andres on LinkedIn.