12 Best Lending Management Systems for 2025 (Hands-on Review)

The lending software market is evolving fast – because it has to.

Borrowers expect instant decisions. Regulators demand transparency. And competition is fiercer than ever. For lenders, the pressure to modernize isn’t optional – it’s survival.

At the center of this transformation?

Choosing the right Lending Management System (LMS).

But here’s the problem: nearly every platform claims to offer automation, compliance, and a seamless borrower experience. In reality? Very few deliver consistently – across origination, servicing, collections, and reporting.

This guide cuts through the noise.

We’ve reviewed the top 12 lending management systems based on what actually matters:

- Configurability and speed

- Compliance and data control

- Automation across workflows

- Integration flexibility

- Onboarding and ongoing support

- Transparent pricing and scalability

Whether you’re a scaling private lender, a digital-first bridge financier, or a large bank with complex legacy systems – we’ll help you find a platform that’s not just fit for today, but future-ready.

Let’s dive in.

📘 Free Checklist: Loan Management Software Buyer’s Comparison Checklist

A practical checklist to verify that you have covered the most critical elements for your business when choosing a new loan management software. Simplify your process by comparing vendors side-by-side.

Top 12 Lending Management Systems for 2025

Below are the platforms making the biggest impact this year – ranked not just by features, but by how well they support real lenders across key categories like configurability, automation, compliance, and support.

We’ll cover:

- Who each system is best for

- Key differentiators

- Limitations to consider

- Pricing overview

- Real-world use cases

1. LendFusion – Best for Fast, Configurable Lending Models

LendFusion is a modern lending management system built specifically for specialist lenders. Whether you’re offering bridge loans, auto-finance, or consumer loans, LendFusion gives you the tools to originate, service, and scale – without the delays or bloat of enterprise platforms.

Key Features

- Modular architecture tailored to your lending model

- Powerful decision engine with rules-based automation

- Built-in audit trail, investor reporting, and document workflows

- Fully GDPR-compliant, EU-hosted infrastructure

- Customer portal and API integrations included as standard

Target Users

LendFusion is ideal for scaling lenders managing between £10M and £100M in loan volume – especially in property, private credit, or digital-first lending. It’s a strong fit for teams replacing Excel-based workflows, legacy CRMs, or overly complex enterprise systems.

Pros

- Fast, Configurable Setup – Go live in under 3 months with full control over workflows, loan types, and data flows.

- Transparent, Flat Pricing – All features included; no per-seat fees or surprise costs.

- Built for Regulated Lenders – Full audit trail, secure EU hosting, and compliance-first architecture.

Cons

- Not for Very Large Institutions – Larger banks may seek bigger vendors with 20+ year track records.

- Focused Scope – LendFusion is purpose-built for lending – not a full banking core.

- Requires Focused Implementation – Teams should commit time during setup to get full value.

Pricing

Plans start from €1,659/month, with scaling tiers based on portfolio size. All features, support, and integrations are included.

Top Tip: LendFusion’s modular system means you can tailor everything – from fees to repayments to investor visibility – without building from scratch.

See LendFusion in action → Book a personalized demo and discover how specialist lenders are scaling faster – without the enterprise baggage.

2. LoanPro – Best for API-First Lending Infrastructure

LoanPro is a powerful lending platform built with developers in mind. It’s designed for tech-forward lenders who want full programmatic control over their servicing engine and lending logic. From repayment schedules to borrower data structures, everything is configurable via API.

Key Features

- RESTful APIs and webhooks for deep integration

- Custom logic for loan terms, payments, and delinquencies

- Real-time data sync across systems

- Loan lifecycle automation via modular servicing layers

- Sandbox environment for rapid prototyping

Target Users

LoanPro is ideal for fintech lenders and large lending operations with in-house engineering teams. If you’re building proprietary borrower experiences or need to embed servicing into an existing product, LoanPro offers unmatched control.

Pros

- Highly Programmable – Dev teams can control nearly every system behavior through a flexible API layer.

- Scales with You – Handles complex loan portfolios and high transaction volumes with ease.

- Modular Servicing Tools – Use what you need – from payment orchestration to delinquency workflows.

Cons

- Steep Learning Curve – Initial implementation requires development time and technical expertise.

- Not Plug-and-Play – No prebuilt flows or templates for non-technical users.

- Limited UI for Ops Teams – Teams without engineering support may find usability challenging.

Pricing

Custom pricing based on volume, integrations, and feature requirements. Typically suited for mid-to-large lenders with dev resources.

Top Tip: LoanPro is best when used as a “servicing engine” under the hood of your own front-end or custom UX.

3. HES FinTech – Best for Custom Origination and Workflow Automation

HES FinTech is a modular lending platform that excels in fast deployment and tailored loan workflows. It’s especially strong for lenders who need end-to-end automation – from borrower onboarding and decisioning to servicing and collections – all wrapped in a configurable UI.

Key Features

- Drag-and-drop loan builder with flexible logic

- White-label borrower and investor portals

- AI-powered credit scoring (optional module)

- Workflow automation for origination, servicing, and collections

- Full-cycle lending engine with customization support

Target Users

HES FinTech is well suited for lenders launching new products, entering new markets, or replacing fragmented legacy tools. It’s used by consumer finance firms, BNPL providers, SME lenders, and leasing companies that want speed without sacrificing flexibility.

Pros

- Launch Fast, Scale Later – Go live in weeks, then evolve the platform as your business grows.

- Tailored Lending Journeys – Customize flows, documents, and borrower experiences with precision.

- Supports Niche Products – Great for non-standard lending models like leasing, payday, and installment.

Cons

- Less “Out-of-the-Box” – Some features require custom implementation or scoping.

- Reporting Gaps – Deep analytics and portfolio insights may need additional setup.

- Ongoing Custom Work – You’ll likely need support hours for system tweaks post-launch.

Pricing

HES LoanBox pricing typically ranges from €20,000 to €70,000 depending on modules and complexity. Monthly licensing follows implementation.

Top Tip: HES is ideal if you’re building something unique and want a technology partner – not just a software vendor.

4. TurnKey Lender – Best for Pre-Built Lending Workflows

TurnKey Lender is an all-in-one platform designed for lenders who want to launch fast with pre-configured workflows and minimal development overhead. It handles origination, decisioning, servicing, collections, and reporting in one package – powered by its own proprietary decision engine.

Key Features

- AI-powered credit decisioning

- Out-of-the-box workflows for consumer, SME, and embedded lending

- Role-based access and borrower portals

- Loan servicing, collections, and document management

- Multi-tenant cloud deployment

Target Users

TurnKey Lender works best for small to midsize lenders, fintech startups, and embedded finance providers who want a fast, plug-and-play LMS with broad feature coverage and minimal IT burden.

Pros

- Fast Deployment – Launch in under 30 days using built-in templates and logic.

- AI-Powered Underwriting – Smart credit decisioning with continuous learning.

- End-to-End Coverage – Handles origination to collections in one tool.

Cons

- Less Configurable at Scale – Pre-built logic limits flexibility for niche or complex models.

- Opaque Pricing Model – Costs scale per user and per feature.

- Vendor Lock-In Risk – Custom changes often require paid support from TurnKey.

Pricing

TurnKey Lender offers custom pricing based on user volume and required modules. Expect monthly costs to rise as your business scales.

Top Tip: Ideal if you’re an early-stage lender or launching a new product – less so if you need deep configuration or full control.

5. BrightOffice – Best for UK-Based SME Lenders

BrightOffice is a UK-centric loan management system that focuses on helping small to medium-sized lenders streamline origination, document handling, and regulatory compliance. It’s especially strong in affordability, document management, and simplicity – ideal for teams without large IT departments.

Key Features

- Built-in document management system (DMS)

- Loan origination and servicing tools

- Simple reporting and compliance tracking

- Cloud-based deployment

- Designed with UK regulatory needs in mind

Target Users

BrightOffice is ideal for SME lenders and financial service providers in the UK who want a straightforward, easy-to-use platform without enterprise-level pricing or infrastructure.

Pros

- Affordable Entry Point – Low monthly fees and scalable pricing make it attractive for smaller firms.

- User-Friendly Interface – Minimal training required; teams can get up and running quickly.

- Integrated DMS – Strong document tracking and compliance features out of the box.

Cons

- Limited Scalability – Not ideal for larger lenders or those planning rapid expansion.

- Fewer Advanced Features – Lacks modern automation and AI functionality seen in newer platforms.

- Customization Gaps – Limited options for tailoring workflows or integrations to unique lending models.

Pricing

Starts from approximately €995/month, with options to scale based on loan volume and additional features.

Top Tip: A great fit for UK-based lenders managing modest portfolios – just know you may outgrow it as your business evolves.

6. ApPello – Best for Custom Workflow Automation

ApPello is a digital lending platform built for banks and financial institutions that require end-to-end control over the loan lifecycle. Known for its modular structure and strong automation capabilities, Appello supports personal loans, mortgages, SME lending, and more – making it a fit for lenders with diverse product lines.

Key Features

- End-to-end loan origination and servicing

- Advanced workflow and approval automation

- Built-in credit risk and KYC tools

- Modular system for tailored deployments

- Support for multi-product, multi-jurisdiction lending

Target Users

ApPello is best suited to mid-size and large lenders with internal tech resources. It’s ideal for those seeking to digitize traditional lending processes or build fully customized workflows.

Pros

- Advanced Workflow Automation – Lets you fully automate the lending journey, reducing manual overhead and approval times.

- Modular Flexibility – Lenders can choose and configure only the features they need.

- Multi-Product Support – Handles a wide array of loan types within a single environment.

Cons

- Complex Setup – Implementation can be resource-intensive and time-consuming without internal technical support.

- Higher Upfront Cost – More expensive than basic platforms, especially for smaller institutions.

- Steeper Learning Curve – Teams may need onboarding and training to fully utilize the platform.

Pricing

Typically starts at around €2,000/month, with pricing adjusted based on modules and loan volumes.

Top Tip: ApPello is best for institutions with technical teams that want full control over how their lending platform functions – from origination logic to compliance rules.

7. Finastra – Best for Large-Scale Institutions and Global Compliance

Finastra is one of the most established names in financial software, offering a comprehensive lending management platform tailored to global banks, credit unions, and multinational financial institutions. With a reputation for reliability, Finastra delivers end-to-end lending functionality that spans origination, servicing, compliance, and reporting – at scale.

Key Features

- FusionBanking loan management suite

- Real-time risk monitoring and compliance reporting

- Global regulatory coverage (incl. AML, KYC, Basel III)

- Support for syndicated, consumer, and commercial loans

- API-enabled and cloud-hosted deployments

Target Users

Finastra is ideal for large institutions that require highly secure, scalable infrastructure with embedded regulatory compliance. It’s especially relevant for cross-border lenders managing complex portfolios.

Pros

- Enterprise-Grade Compliance Tools – Includes advanced regulatory reporting, real-time risk analytics, and audit capabilities.

- Scalability for High Volume Portfolios – Built to support vast portfolios across multiple geographies and product types.

- Extensive Feature Set – Highly customizable for everything from retail to syndicated lending, all in one ecosystem.

Cons

- High Cost of Ownership – Typically priced for enterprise budgets, which may exclude smaller lenders.

- Complex Implementation – Requires significant technical resources and onboarding time.

- Overkill for Simple Use Cases – Institutions with more focused or specialized lending models may find it excessive.

Pricing

Custom enterprise pricing, with typical packages starting from €10,000/month depending on deployment and requirements.

Top Tip: If your lending operation spans multiple regions and regulatory regimes, Finastra’s compliance-first approach and enterprise performance may justify the higher investment.

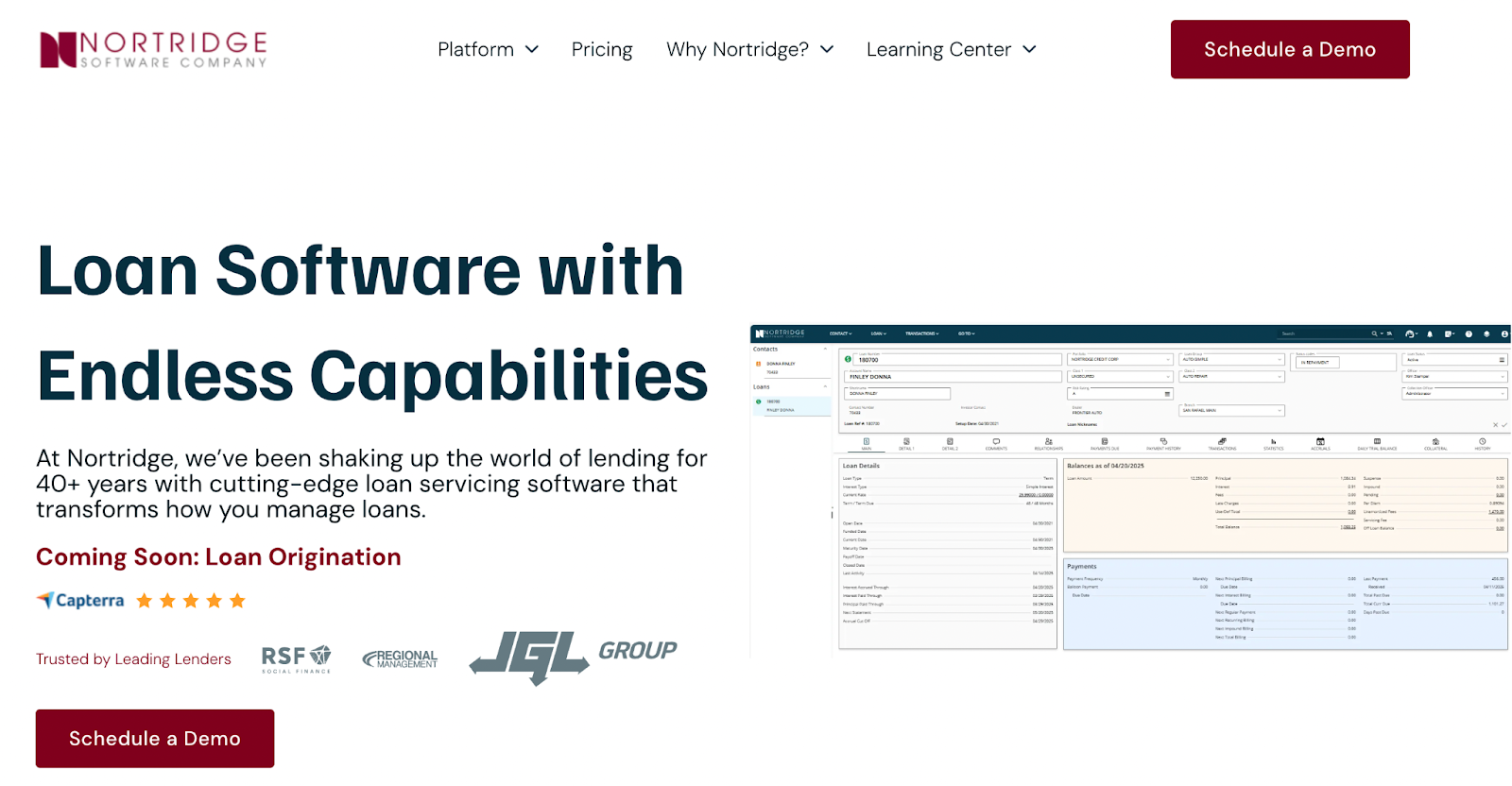

8. Nortridge – Best for On-Premise Control and Deep Configurability

Nortridge is a long-standing player in the loan management software space, known for its highly configurable platform and robust on-premise capabilities. With decades of evolution, it caters to financial institutions that need total control over data, infrastructure, and loan processes.

Key Features

- On-premise or cloud deployment

- Complex rules engine and custom calculations

- Multi-loan product support (consumer, commercial, real estate)

- Advanced accounting and escrow functionality

- Rich reporting and audit trail tools

Target Users

Nortridge is best suited for mid-sized to large lenders – especially credit unions, banks, or niche lenders – with in-house IT teams that want to tailor every aspect of the system to their needs.

Pros

- Maximum Infrastructure Control – Offers on-premise deployment and granular system access, ideal for regulated or highly secure environments.

- Flexible and Feature-Rich – Deep functionality across diverse loan types, complex portfolios, and accounting requirements.

- Proven Track Record – Trusted by financial institutions for decades, with a stable platform and extensive documentation.

Cons

- Steep Learning Curve – High configurability means more complexity; teams without technical experience may struggle.

- UI Can Feel Outdated – Compared to newer SaaS platforms, the user interface isn’t as sleek or intuitive.

- Setup Requires Time and Expertise – Implementation is typically not plug-and-play and needs technical planning.

Pricing

Quote-based pricing. Depends heavily on deployment model (on-premise vs cloud) and volume of loans.

Top Tip: If data sovereignty, internal hosting, or long-term platform flexibility are top of mind, Nortridge delivers unmatched configurability – just be prepared to invest in onboarding.

9. nCino – Best for Banks and Credit Unions

nCino is an enterprise-grade loan management system built natively on Salesforce, offering end-to-end digital lending capabilities for banks, credit unions, and large financial institutions. Its cloud-first approach and deep regulatory tooling make it a favorite among traditional lenders undergoing digital transformation.

Key Features

- Seamless Salesforce integration

- Loan origination, underwriting, servicing, and portfolio management

- Built-in compliance and audit support

- Real-time reporting and workflow automation

- Mobile-ready borrower and relationship manager portals

Target Users

nCino is designed for established banks, credit unions, and commercial lenders – especially those already using Salesforce as a CRM or digital hub. It’s ideal for institutions with complex approval hierarchies and strict compliance needs.

Pros

- Full Lifecycle Coverage – Manages everything from origination to reporting in one connected cloud environment.

- Deep Compliance Features – Includes KYC/AML support, risk monitoring, and automated audit trails built for regulatory scrutiny.

- Salesforce Ecosystem – Native integration with Salesforce allows custom objects, workflows, and UI components.

Cons

- Requires Salesforce Licenses – Since it’s built on Salesforce, institutions must also maintain separate Salesforce licensing and expertise.

- Enterprise-Level Complexity – Designed for large institutions; smaller lenders may find it overwhelming or resource-heavy.

- Implementation Time – Setup and onboarding are intensive, often taking 6–12+ months with dedicated consultants.

Pricing

Custom quote-based pricing, depending on institution size, Salesforce footprint, and required modules.

Top Tip: If you’re already embedded in the Salesforce ecosystem and want to unify lending and CRM into one workflow, nCino is a powerful solution – but expect enterprise-level implementation.

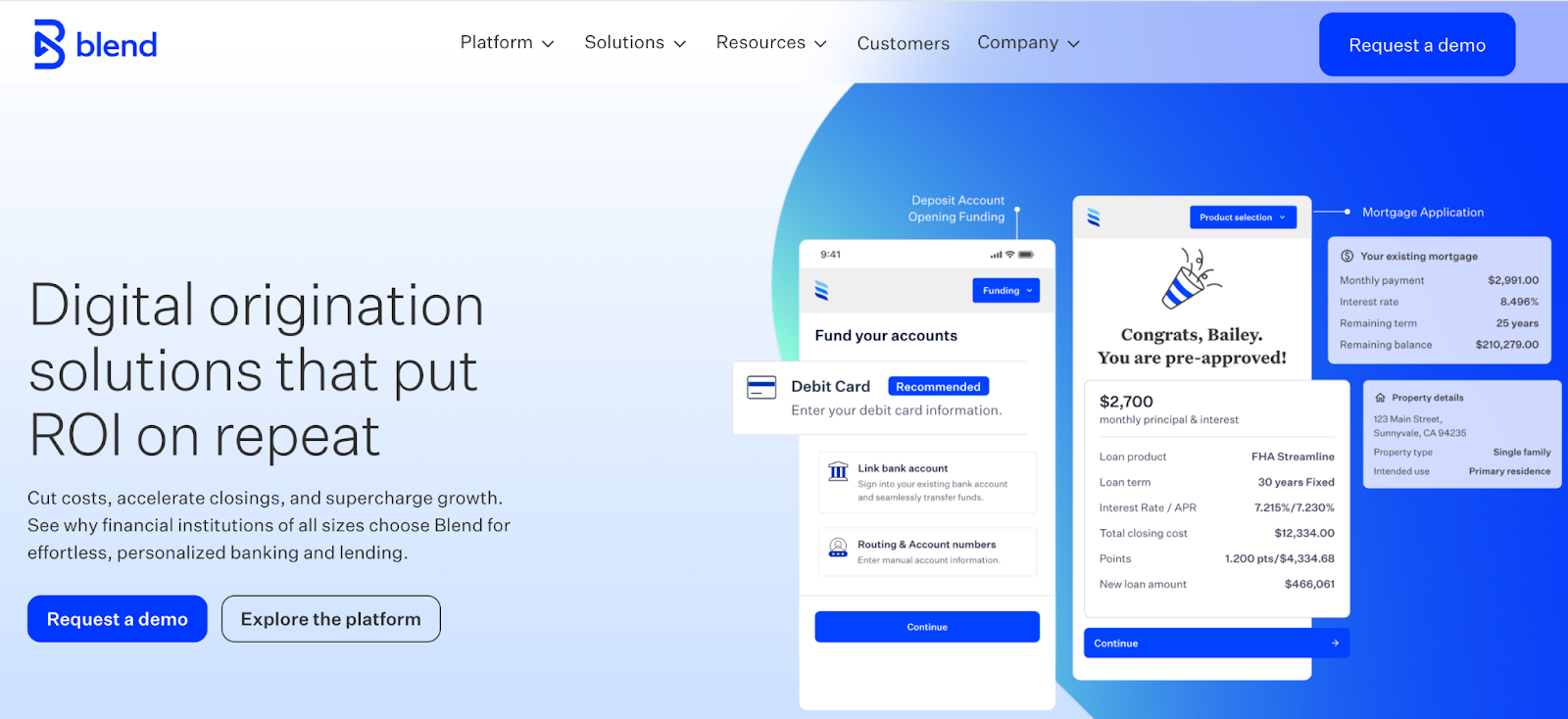

10. Blend – Best for Mortgage and Consumer Lending Automation

Blend is a digital lending platform focused on simplifying loan origination and borrower experience – especially in the mortgage, home equity, and consumer lending space. It helps lenders offer a fast, digital-first experience across web and mobile, while integrating seamlessly with core banking systems.

Key Features

- Streamlined mortgage and consumer loan applications

- Pre-built borrower portals with real-time data entry

- E-signature, document uploads, and identity verification

- Integration with credit bureaus and income verification services

- Automated workflows for underwriting and compliance

Target Users

Blend is ideal for banks, credit unions, and mortgage lenders focused on digital consumer lending. It’s especially suited for institutions modernizing their front-end experience while integrating with legacy cores.

Pros

- Outstanding UX – Blend delivers a frictionless borrower experience, from mobile application to document collection and e-signatures.

- Speed-to-Decision – Built-in data integrations reduce manual review and accelerate approval timelines.

- Trusted by Top Banks – Used by major US banks for home lending, showcasing its scalability and performance.

Cons

- Front-End Focused – Blend shines in origination but requires third-party platforms or custom builds for servicing.

- US-Centric – Best aligned with US lending regulations and infrastructure; limited localization for international lenders.

- Enterprise Pricing – More affordable for large banks; smaller lenders may face budget constraints.

Pricing

Enterprise pricing based on loan volume and features. Requires custom quote.

Top Tip: If your biggest challenge is improving the borrower journey – especially in mortgages – Blend offers an elegant, high-conversion path to full digital lending.

11. Amount – Best for Scalable Consumer Digital Lending

Amount is a fintech infrastructure provider that helps banks and financial institutions launch and scale consumer lending products – fast. Originally spun out of Avant, Amount is known for powering point-of-sale financing, personal loans, and credit card origination with modular APIs and a white-label UI.

Key Features

- End-to-end consumer lending infrastructure

- White-label borrower experience

- Fraud prevention, ID verification, and KYC tools

- Modular APIs for credit decisioning, funding, and servicing

- Integration with major cores and payment processors

Target Users

Amount is ideal for traditional banks and consumer lenders that want to quickly deploy modern digital lending offerings without building from scratch. It’s especially strong for institutions entering POS lending or Buy Now, Pay Later (BNPL) markets.

Pros

- Fast Time-to-Market – Amount’s modular platform helps legacy banks launch digital lending products in a matter of weeks.

- Enterprise-Ready Compliance – Built with KYC, fraud, and regulatory needs in mind – ideal for banks operating under heavy scrutiny.

- Fully White-Label – Delivers a seamless, branded experience across mobile and web, without heavy front-end build work.

Cons

- US-Focused – Compliance, integrations, and product assumptions are tailored to US financial institutions.

- Not for Niche Lenders – The model is best suited to high-volume consumer lending, not specialized products like asset-backed or bridge loans.

- Pricing Reflects Speed – Enterprise-focused packages come at a premium, which may deter smaller fintechs.

Pricing

Custom pricing based on loan volume and modules selected. Typically enterprise-tier.

Top Tip: Want to compete with fintechs without becoming one? Amount gives banks the speed, flexibility, and digital UX to do it – with minimal tech lift.

12. defi Solutions – Best for Auto and Specialty Lending

defi Solutions is a mature, full-suite lending platform trusted by auto lenders, captives, and finance companies across the U.S. With a strong focus on loan originations, servicing, analytics, and document management, defi offers modular capabilities built for scale and compliance-heavy verticals.

Key Features

- Configurable LOS (Loan Origination System)

- Servicing platform with payment workflows and collections tools

- Document and data management

- Compliance tracking and audit support

- Workflow automation and decision rules

Target Users

defi is designed for mid-sized to large lenders in auto finance, powersports, and other specialty verticals. It’s particularly well-suited to lenders with complex approval logic or layered servicing requirements.

Pros

- Vertical Specialization – With deep roots in auto finance, defi brings decades of experience to support lenders with specific needs around titling, collateral, and indirect lending.

- Modular and Scalable – Lenders can implement just what they need – origination, servicing, or both – and expand as they grow.

- Strong Compliance Support – Robust tools for documentation, audit, and risk management make it a good fit for regulated lenders.

Cons

- Primarily US-Centric – Its regulatory tooling, integrations, and workflows are U.S.-focused, with limited EU functionality.

- Legacy Interface – Some users report the UI feels dated compared to newer SaaS entrants.

- Implementation Overhead – Customization is powerful but resource-intensive, often requiring vendor support or internal dev capacity.

Pricing

Quote-based depending on modules selected and scale of operations. Typically targets enterprise budgets.

Top Tip: If you’re in auto or specialty finance and want a platform that’s seen it all, defi offers the depth, scale, and configurability to keep you compliant and competitive.

Comparing Lending Management Systems Side by Side

With dozens of loan management platforms on the market, it can be hard to know which one fits your business best. Some offer rapid setup. Others promise configurability, deep compliance, or powerful automation – but very few get all of it right.

To help, we’ve benchmarked the top 12 loan management systems for 2025 across the key criteria that matter most:

- Ease of use

- Customization options

- Integration capabilities

- Pricing transparency

- Support quality

This table gives you a side-by-side snapshot of how each platform compares – so you can see who leads, who lags, and which one might be the right fit for your lending model.

| Tool | Best For | Pros | Cons | Pricing | Rating |

|---|---|---|---|---|---|

| LendFusion | Regulated, specialist lenders | Feature-rich, EU-hosted, scalable | Learning curve, limited customization | €1,659–€9,999/mo | ⭐⭐⭐⭐⭐ |

| LoanPro | Lenders with tech teams | Flexible, strong integrations | Dev-heavy setup, costly for small orgs | Custom quote | ⭐⭐⭐⭐ |

| HES FinTech | Custom workflows, automation | AI scoring, modular design | Complex setup, enterprise-focused | €20K–€70K+ | ⭐⭐⭐½ |

| TurnKey | Fast deployment needs | All-in-one, built-in scoring | Limited flexibility, opaque pricing | Custom quote | ⭐⭐⭐½ |

| BrightOffice | UK SME lenders | Simple UI, UK-compliant, affordable | Not for high-volume portfolios | From €995/mo | ⭐⭐⭐½ |

| Appello | Custom workflows, risk automation | Configurable, automated workflows | Requires IT, long setup | From €2,000/mo | ⭐⭐⭐ |

| Finastra | Global banks, credit unions | Deep compliance, multi-asset support | High cost, complex for small teams | €10K+/mo | ⭐⭐⭐⭐ |

| Nortridge | Institutions needing control | Powerful rules engine, flexible config | Dated UI, tech-heavy setup | Quote-based | ⭐⭐⭐½ |

| nCino | Banks using Salesforce | Great UI, strong workflow tools | Needs Salesforce, expensive | Quote-based | ⭐⭐⭐⭐ |

| Blend | Mortgage & consumer origination | Top-tier UX, quick to deploy | Weak backend tools | Quote-based | ⭐⭐⭐½ |

| Amount | Digital-first & embedded finance | Modular, partner-friendly | Mostly US-focused | Use case-based | ⭐⭐⭐⭐ |

| defi | Auto & specialty lenders | Industry depth, compliance tools | US-only, legacy UI | Quote-based | ⭐⭐⭐½ |

As you can see, there’s no one-size-fits-all. The best platform depends on your loan types, team size, regulatory requirements, and growth plans. Some solutions like LendFusion offer end-to-end capabilities with transparent pricing, while others like Finastra or nCino cater to enterprise-scale banks with large compliance teams.

Use this comparison as a guide – but always dig deeper into the workflows, support levels, and integration effort required before you decide.

Choosing the Right Lending Management Platform

The loan management software space is more diverse – and more capable – than ever. From LendFusion to defi Solutions and Finastra, there’s no shortage of options. But with that choice comes complexity.

When evaluating platforms, don’t just chase features. Consider how each system fits into your business model, growth plans, and operational maturity.

Whether you’re an SME lender upgrading from spreadsheets or an enterprise institution scaling across markets, the right LMS will free your team from operational drag and help you serve borrowers faster, more compliantly, and with greater confidence.

Ready to streamline your lending operations?

Book a personalized demo with LendFusion and discover why modern lenders across Europe trust us to run their entire loan lifecycle – from origination to exit.

FAQs

What’s the difference between loan servicing vs origination software?

Loan origination software manages the front end of the lending process – everything from applications and credit checks to approvals and documentation. Loan servicing software takes over after the loan is funded, handling payments, interest calculations, customer communication, compliance, and reporting. Some platforms (like LendFusion and LoanPro) offer both in one system, while others specialize in one part of the lifecycle.

Can I switch from Excel or legacy systems?

Yes – most modern LMS platforms are designed to replace spreadsheets, in-house tools, or aging CRMs. Migration typically includes data import, mapping, and support during onboarding. For example, LendFusion offers hands-on migration help for teams moving off Excel or Access-based systems. Expect 4–12 weeks depending on complexity and team resources.

Which platform works best for UK vs US markets?

It depends on your compliance requirements.

- If you’re operating in the UK or EU, platforms like LendFusion, BrightOffice, and HES FinTech offer GDPR-compliant, EU-hosted infrastructure.

- For US-based lenders, systems like LoanPro, defi Solutions, and Finastra are better aligned with US regulations and market practices.

- Always confirm where data is hosted and how the platform handles local compliance (like FCA vs CFPB) before committing.

🚀 Ready to Take Your Lending Business to the Next Level?

Download our Loan Management Software Buyer’s Comparison Checklist and discover all the nuances to consider when shopping for a loan management platform. Identify, evaluate, estimate, compare.

No fluff — just practical examples, templates, and expert tips.

No sign-up required. Just download and start improving your lending business today.

Vahuri Voolaid, COO

Vahuri is the Chief Operations Officer at LendFusion. Vahuri has 9 years of experience in fintech with loan management software as a product owner and an MBA with a specialisation in IT management.

Connect with Vahuri on LinkedIn.