The Hidden Cost of Manual Loan Servicing (and How to Fix It)

If you’re still managing parts of your loan servicing in spreadsheets or across a patchwork of disconnected tools – you’re not alone.

For many lenders, especially in the specialist and mid-market space, manual processes have become the default: familiar, flexible, and just manageable enough to avoid a full overhaul.

But here’s the truth: what feels like a short-term fix is likely holding your entire operation back.

Manual servicing doesn’t just slow you down – it introduces hidden costs across your entire lifecycle. From time lost to double entry, to the risk of missed repayments or faulty interest calculations, the damage compounds.

And the longer you delay modernization, the harder it becomes to scale without adding overhead – or increasing risk.

In this article, we’ll break down where manual processes still live, what they’re really costing you, and how loan management software is helping lenders automate, align, and grow with confidence.

Where Manual Still Rules (and Why That’s a Problem)

Many lenders are still handling key parts of their loan lifecycle manually. It’s rarely a conscious choice – it’s a legacy of growth.

What started as “just a few spreadsheets” evolves into a complex web of stopgap tools, custom-built systems, and team-specific workarounds. Before long, you’ve got servicing spread across Excel, email, your CRM, and someone’s Google Doc.

Here are the most common places manual friction creeps in:

- Repayment tracking handled in shared sheets

- Interest calculations done in Excel macros

- Investor reporting manually compiled from multiple systems

- Document generation copy-pasted from templates

- Borrower updates scattered across inboxes

The problem? These processes don’t scale. Each one becomes a risk vector: for delays, for errors, and for misalignment between teams. And as volumes grow, so does the fragility.

In specialist lending, where structures are already complex and compliance is tight, the cost of a single mistake isn’t just operational – it’s reputational.

The Real Cost of Manual Work

Manual workflows don’t just chew up hours – they bleed your business in more ways than you might realize:

Lost Productivity

Your operations team can spend 20–40% of their week on routine data entry, reconciliation, and reporting tasks. That’s time taken away from high-value activities like optimizing credit decisions, sourcing deals, or improving borrower experience.

Slower Revenue Cycles

Every manual approval or disbursement process adds days – or even weeks – to your loan cycle. Delays in funding mean lost interest revenue, slower reinvestment, and frustrated borrowers who can – and will – look elsewhere.

Increased Error Risk

Human errors in spreadsheets or manual entries can lead to miscalculated interest, missed repayments, or incorrect investor statements. Each mistake requires time-consuming corrections, damages trust, and raises compliance red flags.

Hidden Compliance Gaps

A patchwork of tools makes audit trails incomplete. If regulators or auditors ask for transaction histories, you may struggle to provide consistent, timestamped records – putting your entire operation at risk of fines or reputational damage.

Team Burnout

Repetitive, manual tasks aren’t just boring – they’re demoralizing. High churn in servicing teams drives recruitment costs up and erodes institutional knowledge, creating a vicious cycle of training and turnover.

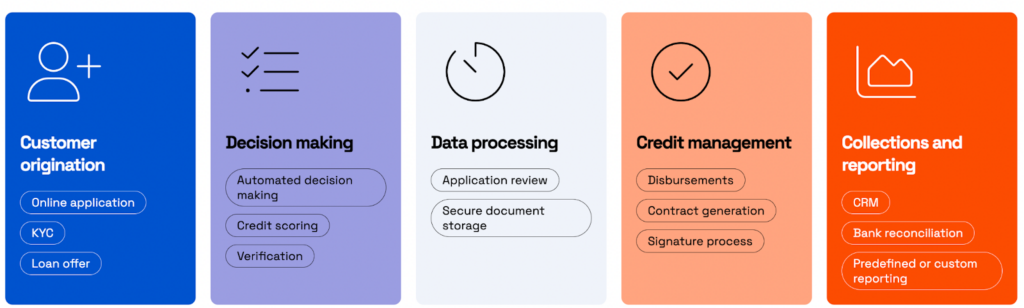

What Modern Loan Servicing Looks Like

The right loan servicing platform doesn’t just digitize what you’re already doing; it redefines how fast, accurate, and scalable your operations can be.

Single Source of Truth

Everything from borrower records and payment schedules to investor reports lives in one place. No more bouncing between Excel, legacy systems, and shared drives. When your data is centralized, your team works faster – and smarter.

Automated Workflows

Loan events trigger actions: interest is calculated, payments are reconciled, statements are generated, emails are sent. No one has to remember to “update the spreadsheet” on Friday. The system does it in real time.

Instant, Audit-Ready Reporting

Need a breakdown of repayments for an investor? Or a regulator asking for transaction trails? You can generate structured, timestamped reports in seconds – with confidence that the data is clean and complete.

Built-In Compliance

Modern servicing platforms are designed with compliance in mind. That means GDPR alignment, permission controls, structured audit logs, and workflows that reduce risk instead of adding to it.

Better Borrower Experience

When your internal processes run smoothly, your customers notice. Automated comms, faster disbursements, and self-serve tools give borrowers the experience they expect – without extra work for your team.

The Business Case for Leaving Manual Behind

Switching from manual servicing to a modern, automated platform isn’t just a technical upgrade – it’s a high-leverage business move. The return on investment shows up fast and across every layer of your operation.

1. Fewer Headcount Hires

Manual servicing eats up hours with tasks that should never touch human hands. By automating repayments, reporting, document generation, and borrower comms, lenders can scale volume without scaling team size. You’re not just saving salaries – you’re protecting focus.

2. Faster Loan Cycles

Speed matters. With automation, loans move from application to disbursement faster – because decisions, verifications, and approvals aren’t bottlenecked by fragmented systems or spreadsheet handovers. That means better borrower experience and more deals closed per month.

3. Better Investor Confidence

Investors want clarity. When your portfolio is tracked in real-time, returns are calculated accurately, and reports are delivered on time (and error-free), confidence increases. That leads to easier capital raising and stronger long-term relationships.

4. Higher Data Trust

When your data lives in a single, structured system – not scattered across ten spreadsheets and three inboxes – you eliminate blind spots. That means faster audits, fewer compliance headaches, and better internal decisions.

5. Scalable Growth

Ultimately, modern servicing creates leverage. You free up internal resources, reduce reliance on patchwork tools, and build the operational muscle to grow faster – with less chaos. The difference between a team that’s just “keeping up” and one that’s truly scaling? It often comes down to the platform underneath.

It’s Not About Replacing Your Team. It’s About Unlocking Them.

Manual loan servicing doesn’t just slow your processes – it holds your entire business back.

The hours your team spends juggling spreadsheets, reconciling data, and building reports could be reinvested in what actually moves the business forward: faster lending decisions, cleaner operations, and better borrower experiences.

Automation isn’t about cutting corners. It’s about removing the friction that prevents growth. And the lenders that are scaling fastest today? They’ve already made the switch.

Want to see LendFusion in action? Book a personalized demo or explore our solutions hub to see how LendFusion helps modern lenders streamline operations – without adding complexity.

Vahuri Voolaid, COO

Vahuri is the Chief Operations Officer at LendFusion. Vahuri has 9 years of experience in fintech with loan management software as a product owner and an MBA with a specialisation in IT management.

Connect with Vahuri on LinkedIn.